Timber Markets by State

Stumpage prices are not set nationally or even statewide — they are set by the mills within hauling distance of your tract. The same stand of pine can bring meaningfully different money in two counties an hour apart, depending on which mills are buying, what they consume, and how much competing timber is on the market. Below is a brief orientation to the major timber states of the U.S. South. When we prepare your estimate, we price your timber against your local market, not a state average.

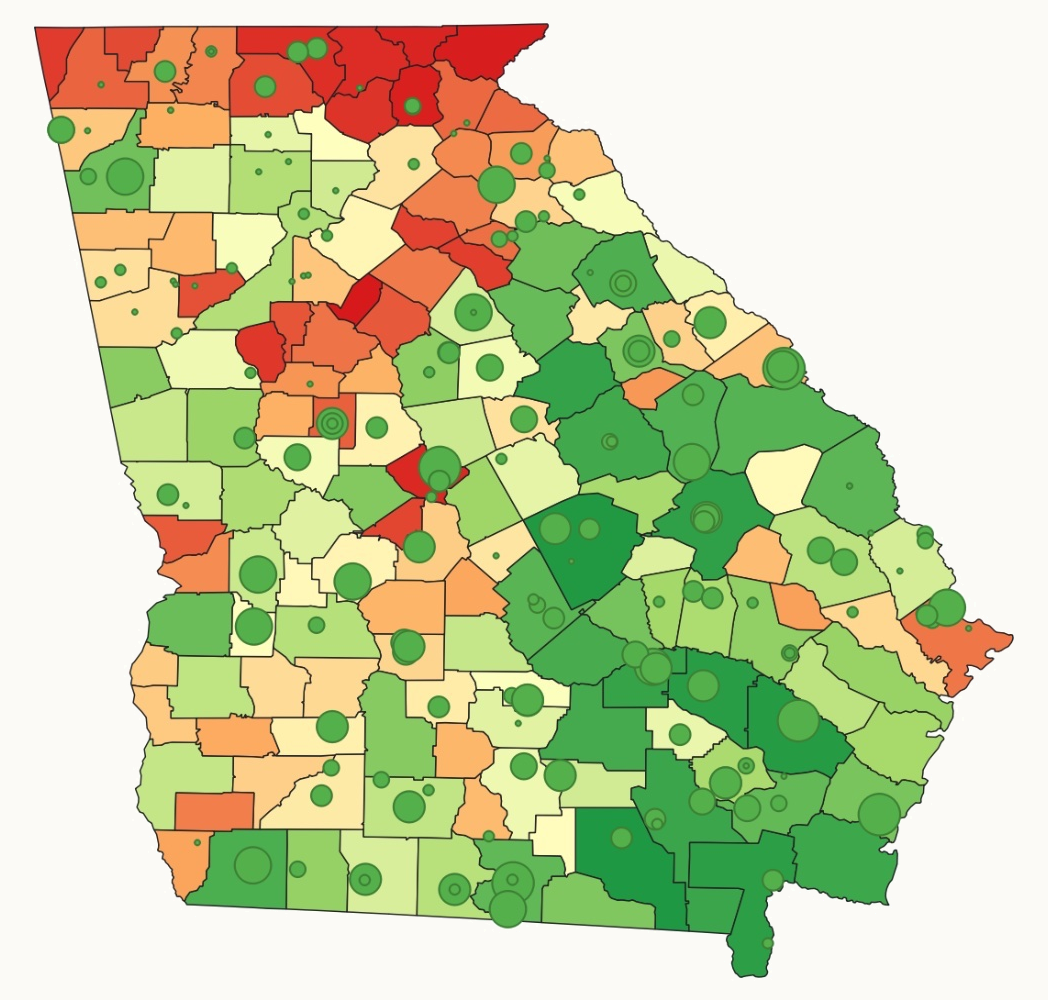

Georgia

Consistently the leading timber-producing state in the nation, with commercial timberland across nearly all of its 159 counties. Planted loblolly and slash pine dominate the Coastal Plain and middle Georgia; the state supports a dense network of pulp and paper mills, sawmills, and pellet facilities. Demand is generally strongest in the southeastern and east-central parts of the state.

Georgia county-level timber demand (green = high, red = low) and active timber-consuming facilities, with markers sized by capacity. We maintain this market intelligence for the regions we serve.

Alabama

One of the most heavily forested states in the country, with strong pine plantation acreage and a deep base of pulp, paper, and lumber capacity. Markets are generally competitive across much of the state, particularly in the south and west.

Florida

Commercial timber is concentrated in the Panhandle and north Florida, dominated by planted slash and loblolly pine. Markets thin out quickly moving south; proximity to the Georgia–Florida mill corridor matters a great deal to price.

South Carolina

A strong pine state with significant pulp and sawmill capacity, particularly in the Coastal Plain. Hurricane and salvage events periodically move local markets, which makes timing and local knowledge especially important.

North Carolina

A mixed market: planted pine in the Coastal Plain, substantial hardwood resources in the Piedmont and mountains. Hardwood quality and species mix drive wide value ranges from tract to tract.

Mississippi

Heavily timbered with extensive pine plantations and a long history of family timberland ownership. Mill capacity is broad, and competitive sealed-bid sales are a well-established practice.

Louisiana & East Texas

The western Gulf market — strong pine plantation country with major lumber and pulp capacity. East Texas in particular has seen significant sawmill investment; haul distance and mill specialization drive local differences.

Arkansas, Tennessee & Virginia

Arkansas combines strong pine markets in the south with hardwood in the north. Tennessee and Virginia are predominantly hardwood states where species, grade, and access drive value, and where careful marketing matters even more than in pine markets.

These descriptions are a general orientation, not a market report. Conditions change with mill openings and closures, weather and salvage events, and broader demand for lumber, pulp, and energy wood. For what is happening in your county right now, request a free estimate and we will give you a current, local answer.